Source: RoseAnn DeMoro on Twitter.

The downside of Medicare for All is that government spending will increase. Various studies indicate that overall spending will be less.

Source: RoseAnn DeMoro on Twitter.

The downside of Medicare for All is that government spending will increase. Various studies indicate that overall spending will be less.

Obamacare is a flawed system. It gives for-profit insurance companies a captive market. It fines people for not buying insurance that they can’t afford, or that does them no good because of the large co-pays.

It is more expensive than the obvious alternative, which is a single-payer system, otherwise known as Medicare for all.

But the Congressional Republicans reject the obvious alternative. What they’ve come up with is worse.

This chart is based on estimates by health researchers as to how many people die each year as a result of lack of health insurance, plus estimated by the Congressional Budget Office of how many people will be uninsured under the House Republicans’ American Health Care Act versus the Democrats’ Affordable Care Act.

It’s a cumulative chart. The estimated number of deaths are the same year by year.

Poor People Need BETTER Insurance Than the Rest of Us, Not Worse by Doug Muder for The Weekly Sift.

President Donald Trump, in his first day in office, issued an executive order to cripple the administration of the Affordable Care Act.

The order (1) forbids administrators to issue any new order or regulation that imposes new costs on states and (2) authorizes administrators to suspend any order or regulation that imposes undue costs on individuals or states.

The order (1) forbids administrators to issue any new order or regulation that imposes new costs on states and (2) authorizes administrators to suspend any order or regulation that imposes undue costs on individuals or states.

The limitations are that the change has to be permitted by law and that there have to be advance note and public comment on the changes if the law requires it.

That may sound relatively harmless, but the ACA is so complicated that it is hard to make it work and easy to make it cease functioning—like removing a couple of bolts from a highly complex machine.

Here are some of the things reporters said could happen under Trump’s executive order:

Another thing the Trump administration could do is to stop defending a lawsuit by the House of Representatives challenging the legality of a program to reimburse insurers for providing subsidies for low-income patients. The program was authorized by law, but no money was ever specifically appropriated for it. The U.S. District Court agreed the program is illegal; the case is now on appeal to the U.S. Court of Appeals.

Economics professor David Ruccio points out that, since the previous recession, the American middle class has been cutting back on spending—on everything except medical care.

The Affordable Care Act was supposed to not only make medical care more widely available, but to make it affordable. This hasn’t happened. I think this is partly due to opposition by Republican governors and congressional representatives, but largely due to flaws in the law itself.

It’s a well-known fact that we Americans pay more for medical care and get less benefit than citizens of any other industrial nation.

Source: Charles Gaba’s Blog

Hat tip to Avedon’s Sideshow

A blogger named Charles Gaba has figured out that, under Obamacare, slightly over 294 million Americans now have health insurance, but 29 million are still without—about 9 percent of the population.

The striking thing to me is how much work he had to do to come up with a plausible estimate. I would have thought that the U.S. Department of Health and Human Services had that figure on a web site somewhere.

I would have thought that, in general, President Obama would do more to ensure careful management of his signature reform, given how complicated it is and given how determined his Republican political enemies are to make it fail.

Click on Charles Gaba’s Blog for a detailed breakdown of the figures and an explanation of how he arrived at them, and a larger, higher-resolution version of the chart.

When the Affordable Care Act was enacted five years ago, I was aware of its flaws, but I thought it represented an advance over what we had before.

When the Affordable Care Act was enacted five years ago, I was aware of its flaws, but I thought it represented an advance over what we had before.

Obamacare did give access to health insurance to millions of Americans, including people with pre-existing conditions, who otherwise wouldn’t have been able to get it. The tradeoff was that it created a captive market for the health insurance companies to provide bad insurance.

My e-mail pen pal Bill Harvey sent me a link to an article by a Dr. John P. Geyman for the International Journal of Health Services which, in my opinion, sums up the problems with Obamacare very well.

Dr. Geyman thinks the answer is a single-payer health system, financed by taxes which covers everyone. Such a system would be cheaper for most people than a private system because it simplifies administration and subtracts the need for profit.

One reason why such a system wasn’t considered in 2010, in addition to the entrenched power of pharmaceutical and health insurance lobbyists, was that many Americans were satisfied with their existing insurance and didn’t want to risk an unknown system.

Now private insurance has changed for the worse for most people. Unfortunately, it will be very natural for people to see the inadequacies of Obamacare as an argument against any government health insurance plan at all.

LINK

A Five-Year Assessment of the Affordable Care Act: Market Forces Still Trump the Common Good in U.S. Health Care by John P. Geyman for the International Journal of Health Services. (Hat tip to Bill Harvey)

I’ve long been of two minds about Obamacare. Sometimes I think it is a complete mess and sometimes I think that, despite its complexity and obvious flaws, it will be of net benefit to the American public.

There is one group of people who’ve made up their minds about it, and that is the Republicans who are determined to prevent implementation of the Affordable Care Act by any means necessary.

If they believed the law is as terrible as they say they do, the smart political strategy would be to allow the law to go into effect, allow the public to see how bad it is and then move to repeal or amend.

The only explanation is that they don’t dare let this happen because they think that, once Americans experience the new law in operation, they will embrace it and vote for Democrats forevermore in gratitude.

Jon Perr explained for Daily Kos why Obamacare does not fix the dysfunctional U.S. health insurance system.

On January 1, 2014, the Affordable Care Act went fully into effect. But for all of the furious fighting over the law these past five years, Obamacare was always an evolutionary reform grafted onto the existing American health care system. The Medicaid public insurance program has been extended to roughly four million lower income Americans so far. About two million more people have purchased private insurance, many of them aided by subsidies from Uncle Sam.

And while many (though not all) of the worst abuses that let insurers pad their profits by denying or dropping care for the sick have been banned, the edifice of private insurance remains largely intact.

Far from a “government takeover of health care,” Obamacare preserves all of the hallmarks—private insurance companies, private hospitals, private doctors, and the patchwork of different systems for veterans, seniors, workers, and the poor—that define the American model of health care provision.

Click on Why the U.S. should treat health care like a utility, not a market to read Perr’s full article. Hat tip for to Bill Elwell for the link, which is the source of the charts.

Liberals like to point out that the Affordable Care Act’s individual mandate is the same as a proposal by the right-wing Heritage Foundation. That is, everybody has to buy insurance from for-profit companies, but insurance in theory becomes affordable because the cost is spread out over a whole population of rich and poor, sick and healthy and old and young.

I, too, sometimes fall into the trap of saying President Obama’s plan as a whole is a warmed-over Republican plan, but, as Scott Limieux pointed out on his Lawyers, Guns and Money blog, this is not really so.

Of course it remains to be seen whether there really will be strict, federally enforceable consumer rights, or whether the ACA will simply create a new captive market for the health insurance industry.

And the historic expansion of Medicaid, which was a key part of the ACA, was sabotaged by the Supreme Court and Republican state governments, although that is not Obama’s fault and may eventually be overcome.

The important thing about the ACA is that there is no longer any point in speculating about its impact. It is the law and will remain law until at least 2016, and that will be plenty of time to see whether it does more good than harm.

Not long after I voted for Barack Obama in 2008, I came to realize that his priorities were different from what I thought they were. And I soon saw that his health reform plan was deeply flawed and hard to implement. But I nevert, until now, thought that he was incompetent.

The Affordable Care Act is President Obama’s signature domestic achievement. Compared to Medicare for all (single payer) or his own proposal for a public option, it is hugely complicated. Moreover there are political enemies in state governments that want to make it fail, and special interests in the pharmaceutical and health insurance industries that want to milk it for their own benefit.

The Affordable Care Act is President Obama’s signature domestic achievement. Compared to Medicare for all (single payer) or his own proposal for a public option, it is hugely complicated. Moreover there are political enemies in state governments that want to make it fail, and special interests in the pharmaceutical and health insurance industries that want to milk it for their own benefit.

Under these circumstances, wouldn’t you think that he look for the smartest and most capable information technology manager he could find and give that person complete authority? With his connections in Silicon Valley industry, he wouldn’t have had trouble finding such a person. But evidently not.

President Obama’s right-wing opponents accuse him of creating “czars” to oversee government programs, but this was a case where a “czar” was necessary and sadly lacking.

And wouldn’t you think that he would check on the progress of the program early and often? The President, after issuing a non-apology apology, said, “I was not informed directly that the web site would not be working the way it was supposed to.” This is a statement worthy of George W. Bush. Why was he not informed.

During the George W. Bush administration, I blamed President Bush, Vice President Dick Cheney and Karl Rove for mistaking campaigning for governing, and public opinion polls for reality. But when individuals so different in background and personality as George W. Bush and Barack Obama exhibit the same flaws, I have to think there is something deeply wrong with the U.S. political culture that goes beyond the character traits of individuals.

Many more Americans want to keep the Affordable Care Act or make it stronger (47 percent) than want to repeal it or replace it with a Republican alternative (37 percent). I do not venture to predict how they will think a year from now when the technical problems will (presumably) be resolved and the law will go into force.

Many more Americans want to keep the Affordable Care Act or make it stronger (47 percent) than want to repeal it or replace it with a Republican alternative (37 percent). I do not venture to predict how they will think a year from now when the technical problems will (presumably) be resolved and the law will go into force.

House Speaker Nancy Pelosi was right. We won’t really understand what’s in the law until it goes into operation. I am sure that lives will be saved by forcing insurance companies to cover people with pre-existing conditions, and I hope that a lot more people will benefit financially than will be hurt. But even if things work out for the best, Obamacare at best is deeply flawed.

New Medical Gatekeepers. The ACA makes for-profit insurance companies the gatekeepers between physicians and patients. The only way to have a doctor of your choice is to find an insurer that has that doctor on its roster.

Insurance companies get even greater leverage than they have now in imposing a corporate business model on physicians. A physician who spends too much time on sick and needy patients will not be cost-effective from a business standpoint, and may be dropped from the roster. This isn’t new, but Obamacare locks it in.

Controlling the Wrong Costs. President Obama is cutting Medicare reimbursements to health care providers. At the same time he has locked for-profit insurance companies into the system, and declined to negotiate with pharmaceutical companies to lower drug prices.

This is a typical example of how things work in American life nowadays. The people who do things that create value are being squeezed. The people who extract profits from what others create are left untouched.

It may well be that health care providers are overcharging Medicare. I don’t have the facts and figures to express an informed opinion either way. It does seem to me that, for example, $800 is a lot to charge for an ambulance ride. But I might think differently if I knew what it cost to pay for and maintain a fully-equipped ambulance, to pay for and maintain the ambulance station, and what it costs to train and pay ambulance crews and keep them available 24 hours a day 7 days a week.

But it is obvious that there is no public benefit in going through a for-profit insurance company to get a benefit mandated by government, or in paying more for a drug than foreigners pay for the same drug.

Complexification. One of the problems with the American health care system—a mixture of employer-based insurance, individual insurance, Medicare, Medicaid and veterans’ benefits—was its complexity. The Affordable Care Act makes it more complicated, and I think that is the main reason why the Exchanges and sign-up system don’t work.

There would not be any problems in signing up if Congress had enacted a single-payer plan (Medicare for all) or, if that was not feasible, simply expanded Medicare or federalized and expanded Medicaid. The voluntary public option proposed by Senator Barack Obama in 2008 would have been more difficult, but still simpler than what was advocated.

Even though I think the Affordable Care Act is a bad law, I’m opposed to most of the people who oppose the law.

Most opponents of the law are against it because they don’t agree with having the government guarantee a minimum level of medical care to all. I’m opposed to the law because I don’t think it will come anywhere near to accomplishing that purpose.

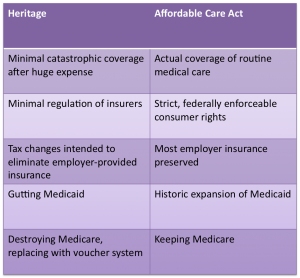

Defenders of the Affordable Care Act point out that it originated as a conservative Republican plan, drafted by the right-wing Heritage Foundation and first implemented by Mitt Romney as governor of Massachusetts.

From my standpoint, that is the problem. I am a liberal Democrat who voted for Barack Obama in 2008, and I did not vote for him in order to advance a conservative Republican agenda.

I’m pretty sure that the Heritage staff did not offer up their plan because they felt an urgent desire to assure health insurance for everybody. I think they proposed their plan as a way to avoid enacting Medicare-for-all, aka a single-payer plan.

The chief merit of the Obama / Heritage plan from the right-wing point of view is that it locks the for-profit insurance companies into the system and gives them a captive market, even though they add no value to medical care. The threat of a universal system would be that there would be no role for the insurance cmpanies.

Back in 2008, the single-payer plan was the mainstream Democratic position. Both Hillary Clinton and John Edwards advocated it in their presidential campaigns. Barack Obama offered a moderate compromise, a public option in which an affordable government insurance plan would be made available, which at the time that seemed reasonable to me.

But as soon as President Obama took office, he embraced the Heritage / Romney plan. His staff ridiculed anybody who took his campaign promise seriously.

If Obama thought that this would bring the Republicans on board, he was sadly mistaken. They reverted to what they really wanted all along, which is to do nothing or take away what we have.

In five years, the former mainstream liberal position has been taken off the table for discussion. The former mainstream conservative position has been redefined as the liberal position. The extreme right-wing position which was not then on the table has been redefined as the mainstream conservative position.

Nobody really wanted Obamacare. It was originally proposed as a lesser evil from the conservative point of view, and it was enacted as being a lesser evil from the liberal point of view. The right-wing Republican goal is to get rid of it altogether. The liberal Democratic goal should be to replace it with something adequate.

The Affordable Care Act is a bad plan. It may be a lesser evil than the system we had before, just as the system we had before was better than nothing at all, but it falls short of what Americans have a reasonable right to expect.

Obamacare creates a captive market for the for-profit insurance companies, which in themselves contribute nothing to the availability or quality of medical care.

It is a form of privatization of social insurance, which creates a bad precident—especially ominous in the light of President Obama’s repeated statements about the need to cut Medicare and Social Security.

By design, it does nothing to control some of the main things that make health care so expensive in the United States. In addition to locking the insurance companies into the system, it allows pharmaceutical companies to charge Americans more than what they charge Canadians and Europeans for identical products. And it complexifies the needlessly complex existing system.

Instead of providing a universal system, it creates a means-tested system where different people give different levels of health insurance, and some are still outside the system.

While the ACA provides subsidies to low-income citizens who can’t afford health care premiums, these may in the long run turn out to be mere pass-throughs that enable insurance companies to raise their rates, just as the Pell grants to college students eventually become mere pass-throughs to the colleges.

And while it assures insurance to many people who previously were denied it, I seriously question whether either competition or federal regulation will guarantee insurance premiums are affordable. Even if government regulators are serious about keeping insurance affordable, there are many ways for companies to game the system, by providing lower levels of care, asking higher deductibles and simply making it difficult to file claims (I have personal experience with the latter).

I do recognize that Obamacare has helped many people and even saved lives. I don’t advocate wiping it off the blackboard and going back to the previous system. But we Americans shouldn’t accept that this is the best we can do.

The cartoon tells how the Affordable Care Act is supposed to work. Insurance companies are mandated to give health insurance to everybody who needs it. Everybody is mandated to sign up for health insurance rather than waiting until they are sick. The government will subsidize insurance for those who can’t afford it.

The problem is that Mr. Insurance Company can game the system. He can raise premiums on Bob, Sam, Dave and Mary. If premiums are limited, he can raise the deductible or restrict coverage—following the principle of raising the price of cereal by putting less cereal in the box.

Instead of shutting down much of the government, Congressional Republicans who oppose Obamacare would have been better advised to let it take its course.

The rollout of Obamacare has been a mess, but, because of the shutdown crisis, this has received little news coverage. Cartoonist Ted Rall wrote last week in his syndicated column about his six-hour struggle to sign up for Obamacare on-line. But the real problem was the Exchange’s menu of choices.

Talk about sticker shock.

NOT affordable. Not, as Obama said, lower than your cellphone bill.

For this 50-year-old nonsmoker, New York State’s healthcare plans range from Fidelis Care’s “Bronze” plan at $810.84 per month to $2554.71 per month. I didn’t bother to look up the $2554.71 one because if I had $2554.71 a month lying around, I’d buy a doctor.

$810.84 per month. $10,000 a year. After taxes. Where I live, you have to earn $15,000 to keep $10,000.

Not affordable. Did I mention that?

The plans offered by New York State do not allow you to go “out of network” for healthcare. In other words, you have to use a doctor in each private insurer’s list, or they don’t pay a cent of reimbursement.

Even worse, the plan “deductibles” — the amount you pay out of pocket each year before your insurer has to cover you for anything at all — are outrageously high.

Fidelis Care Bronze has a $3000/year deductible per person. I’m in pretty good health; it’s a rare year I spend that much on doctors. This is what used to be known as a catastrophic plan: OK if you get hit by a bus but useless for most people living typical lives.

After the $3000/year deductible, Fidelis would pay 50% of your bills. So if you rack up $5000/year in medical bills, you pay $4000 and they pay $1000. Crappy.

via Ted Rall’s Rallblog.

One good part of Obamacare was the expansion of Medicaid, the government health insurance program that serves poor people. But because of a decision by the Roberts Supreme Court, conservative state governments are in a position to block implementation to those who need it most.

Medicare works. It delivers health insurance for less overhead than for-profit plans. If it were up to me, I would replace Obamacare with Medicare for everyone (a single-payer plan). If that wasn’t feasible, I’d lower Medicare’s age limits year by year.

But one of President Obama’s stated goals is to cut spending on Medicare, as well as on Social Security. The net result is leave patients even more at the mercy of the for-profit insurance industry.

Double click to enlarge

The New York Times reported that, thanks to the Supreme Court’s Medicaid loophole and the actions of the governments of 26 mostly Southern states, millions of poor people will be excluded from Obamacare. The article said:

A sweeping national effort to extend health coverage to millions of Americans will leave out two-thirds of the poor blacks and single mothers and more than half of the low-wage workers who do not have insurance, the very kinds of people that the program was intended to help, according to an analysis of census data by The New York Times.

Because they live in states largely controlled by Republicans that have declined to participate in a vast expansion of Medicaid, the medical insurance program for the poor, they are among the eight million Americans who are impoverished, uninsured and ineligible for help. The federal government will pay for the expansion through 2016 and no less than 90 percent of costs in later years.

Those excluded will be stranded without insurance, stuck between people with slightly higher incomes who will qualify for federal subsidies on the new health exchanges that went live this week, and those who are poor enough to qualify for Medicaid in its current form, which has income ceilings as low as $11 a day in some states.

[snip]

The 26 states that have rejected the Medicaid expansion are home to about half of the country’s population, but about 68 percent of poor, uninsured blacks and single mothers. About 60 percent of the country’s uninsured working poor are in those states. Among those excluded are about 435,000 cashiers, 341,000 cooks and 253,000 nurses’ aides.

via NYTimes.com.

Barry Ritholtz on The Big Picture provided this map showing the overlap between those who want to block health insurance for poor people and those who want to shut down the government.

Double click to enlarge

The Affordable Care Act does good things. It extends health insurance to many (but not all) of the uninsured. It forbids denying people health insurance because of a pre-existing condition. Young people can be covered by their parents’ health insurance for longer periods of time.

The Affordable Care Act does good things. It extends health insurance to many (but not all) of the uninsured. It forbids denying people health insurance because of a pre-existing condition. Young people can be covered by their parents’ health insurance for longer periods of time.

The big problem with the law is its complexity. Generally speaking, government is a good mechanism for doing simple, clear-cut things, and a bad mechanism for doing complicated things.

Obamacare is hard to implement, as is seen in all the delays and exemptions in rolling out implementation.

And it is easy to sabotage. The U.S. Supreme Court opened the door for sabotage by striking down a provision requiring expansion of Medicaid, the government health care program for the poor. (I don’t get this. How is it that the Medicaid law is constitutional, but expansion of Medicaid is unconstitutional?)

As a candidate, Barack Obama proposed a simple, workable public option. A public option would be a self-financing government health insurance system that people could join if they couldn’t get private insurance or weren’t satisfied with their current insurance. It didn’t require micro-managing the whole U.S. health care system. But that would have been a threat to the for-profit health insurance industry. For whatever reason, Obama quickly abandoned his plan when he was sworn in as President.

Obamacare does nothing to address the reasons Americans pay so much more for medical care than foreigners do. It disallows the government negotiating with drug companies for lower drug prices, as foreign governments do. It locks in for-profit health insurance, which would play no useful role in a universal health care system. And it does not address the fact that physicians and other specialists have much higher incomes than in foreign countries. As with some of the President’s other initiatives, it leaves me in doubt as to which side he is on.

I agree that some of the reasons for opposing Obamacare are bogus. Employers blame the Affordable Care Act for layoffs and downgrading jobs from full-time to part-time, but I think most of that would be happening without the law.

The best result for Obamacare would be that it results in a net improvement, with the possibility of further piecemeal improvement. The worst is that it would leave many people worse off than before, and discredit the whole idea of universal health care.

I fear Obamacare will be a big unwieldy mess, which ordinary people won’t understand and which the insurance, drug and medical industries can manipulate to their own advantage. But I’m not sure I’m right about this, and I hope I’m wrong.

Click on The GOP’s Self-Defeating ‘Defunding’ Strategy for Karl Rove’s article in the Wall Street Journal.

This opinion poll by Pew Research indicates that more than half of the opponents of the Affordable Care Act think that elected officials should try to make it work as well as possible rather than sabotaging it and making it worse.

Some time back I saw a public opinion poll that indicated that some of the opponents of Obamacare oppose it because (like me) they would prefer a single-payer system (Medicare for everybody) or a public option as a voluntary alternative to private insurance. I wasn’t able to find the poll in a Google search.

[Update: In the latest CNN poll, 54 percent of respondents opposed Obamacare, but of that group, 16 percent opposed it because they thought the bill was not liberal enough.]

What I’d be interested in seeing is a current poll of the opponents of Obamacare giving a breakdown as to (1) those who oppose it because they think it won’t provide affordable health insurance to the currently uninsured and (2) those who oppose it because they are opposed in principle to the government spending money to give people medical care. I’d also like to see a breakdown of opponents who would like the government to (a) do more or (b) do less.

But whatever Americans think of the Affordable Care Act, a majority disagree with shutting down the government or risking a default on government in order to prevent it from being implemented.

Click on What Republicans don’t understand about the politics of Obamacare for more from Ezra Klein on the Washington Post’s Wonkblog.

Hat tip to jobsanger.

I don’t see how the Affordable Care Act, aka Obamacare, can work. It’s too complicated. It provides too many openings to game and undermine the system. It doesn’t get at the causes of out-of-control health insurance costs.

There are good things in Obamacare—the provisions that you can’t be denied medical insurance for a pre-existing condition; that grown children continue to be covered by their parents’ policies until age 26; that insurance companies can’t set a lifetime limit for coverage.

But the employer mandate gives an incentive for companies to avoid health insurance costs by cutting workers or cutting hours so that they are exempt from the bill. The individual mandate give the health insurance industry a captive market without any protection against overcharging or underinsuring.

The Republican right wing’s war opposes Obamacare for exactly the wrong reason. They oppose Obamacare not because it can’t achieve it’s stated goal of providing adequate medical care for all Americans, but because they are opposed to that goal.

President Obama actually is helped by the kind of enemies he has. It makes his medical insurance plan seem better than it is. That’s one reason I was willing to give Obamacare the benefit of the doubt when it first was proposed. I thought that anything so vehemently opposed by the likes of Sarah Palin and Rick Perry must have something good about it.

Chief Justice John Roberts handed backers of Obamacare a time bomb in the part of the court decision affecting Medicaid. The whole point of the Affordable Care Act is to provide health insurance to people who can’t afford to pay for it. Expansion of Medicaid coverage of people above the poverty line is an important part of expanding health insurance coverage, and one of the things that made Obamacare palatable to liberals. But Chief Justice Roberts rules that state governments can refuse to expand Medicaid coverage if they wish, and still keep existing Medicaid subsidies.

A number of state governors—all Republicans—have said they’ll exercise their right to refuse to expand Medicaid. I’m in favor of expanding Medicaid, and I wish I could say that this is nothing more than blind partisanship or contempt for the poor. Unfortunately, there are objective reasons why a state governor might be dubious about expanding Medicaid.

The good folks at Think Progress point out that, under the Affordable Care Act, the federal government will pay 100 percent of the cost of Medicaid expansion for the first two years, and 90 percent for the next five years. But what happens after seven years? This is how the federal government has always induced state and local governments to adopt federal programs—offer subsidies that are too enticing to refuse, then gradually pull back after the program has created a local constituency to advocate for it.

Unfunded federal mandates are a big program for state and local governments, and unfunded state mandates are a big problem—I don’t think New York state is alone in this—for state governments. The growing cost of Medicaid, unlike Social Security and Medicare, is a big problem. Part of the practice of my lawyer friend DH is to help middle class retirees gradually give away their wealth to their loved ones so that they can qualify for Medicaid in their declining years. I don’t blame people who want to leave an inheritance rather than have it all eaten up by medical bills, but this isn’t the purpose of Medicaid.

The Obama administration claims there are cost-saving measures that will limit the increase in Medicaid. Fewer people will go to hospital emergency rooms for routine medical care, for example. Maybe so and maybe not—the answer is not obvious. What was obvious from the start was that the complexity of the Affordable Care Act, and the slow timetable for putting it into effect, was sure to guarantee an ongoing struggle.

Click on GOP Governors May Turn Down $258 Billion in Obamacare Funds, Leave 9.2 Million Americans Uninsured for analysis by Think Progress and the source of the map and chart above.

Click on GOP governors may be shafting their own states and constituents for an argument by Greg Sargent of the Washington Post that the Affordable Care Act will actually save states money. The problem with his argument is that they’ll get the benefit of these savings whether Medicaid is expanded or not.

Click on The Obamacare Tax on the Middle Class for an argument by James Kwak on Baseline Scenario that most Americans will not be affected by the Affordable Care Act and that most of those who are affected will pay less for health coverage.

Click on The Dems who might fight “Obamacare” for speculation by Steve Kornacki of Slate about Democratic governors who might refuse Medicaid expansion.

Click on Are Federal-State Grant Programs “Progressive”? for thoughts of Ed Kilgore on the Washington Monthly’s Political Animal blog. [Added 7/10/12]

Mitt Romney was for the individual mandate before he was against it.

Barack Obama was against the individual mandate before he was for it.

When Obama was running in the Democratic primary in 2008 against Hillary Clinton, she favored a single-payer system—essentially Medicare for everybody. Obama as an alternative proposed what he called a public option. Under that plan, everybody would have free choice of health insurance, but those who couldn’t get insurance, or get affordable insurance, from private companies would have the option of enrolling in a government plan open to everyone.

The public option would operate under the disadvantage of having to take the rejects of the private insurance plans. But the advantage of the public option would be that a government plan would not have to take out 20 to 40 percent of premiums to for stockholders’ profits (financial analysts use the term “loss ratio” to describe the percentage of health insurance premiums that actually goes to medical care) nor the burden of calculating risk and deciding who to insure and for how much. I think a public option would have been the best choice.

Once in office, though, President Obama decided to go for a national version of the health insurance plan enacted in Massachusetts when Romney was governor. This would require everyone to buy health insurance, just as everyone has to buy automobile insurance. In theory, this would make it possible to keep premiums down because the risk would be spread among a diverse group of people, rich and poor, healthy and sick. I think this could be better, although I’m not sure it will be better in practice. But the whole point of the plan is that everybody must enroll. If you strike down the individual mandate, you no longer have a universal system—which, to my mind, is the point.

Click on What the flip flops on the individual mandate mean for Dems and Repubs for Don Taylor’s thoughts on The Reality-Based Community web log.

The individual mandate is one part of an extremely complicated law. Click on What exactly is Obamacare and what did it change? for a clear and objective explanation of just what is in the Patient Protection and Affordable Care Act.

Click on What Is a Medical Loss Ratio? The Check Will Be in the Mail for an article in Forbes magazine about high overhead costs of for-profit insurance systems.

The best book I’ve read on the subject of health care reform is T.R. Reid’s The Healing of America, published in 2009, which examines health insurance systems of different countries and compares them to the U.S. system. Click on It’s Not a Socialized World After All for a review of the book. Click on Daily Kos: The Healing of America for a current comment.

Click to view.

I don’t know whether the Affordable Care Act — also known as Obamacare — is a good thing or not. It could be, but I’m not sure it will be. But if the mandate that all individuals buy health insurance is declared unconstitutional, then Congress might as well repeal the whole law and start over.

The problem with U.S. health insurance is that we Americans spend more on medical care than the people of any other advanced nation and, in fact, our government spends more than the governments of most nations, and yet we have 47 million people uninsured.

Candidate Barack Obama proposed an alternative, which he called the public option. The government would set up its own insurance plan which would accept anybody who applied. The theory was that since (contrary to widespread belief) government systems are so much more efficient than for-profit systems, the public option could still compete even if it had to accept people with pre-existing conditions. You could choose between a public option where 5 percent or so of premiums went to overhead, as with Medicare and Medicaid, or a for-profit system where more than 30 percent of premiums went to overhead and profit, or you could opt to pay your medical bills yourself (good luck on that!).

In office, President Barack Obama evidently decided that this was not politically feasible. Instead he supported what became the Affordable Care Act requires everybody to buy health insurance, like it or not, just as state laws require every driver to buy automobile insurance.

In office, President Barack Obama evidently decided that this was not politically feasible. Instead he supported what became the Affordable Care Act requires everybody to buy health insurance, like it or not, just as state laws require every driver to buy automobile insurance.

For-profit insurance companies have an incentive to spend as little as possible on actual medical care. The payout to patients is called the “loss ratio.” The law attempts to get around this by means of regulation. It requires insurance companies to spend 80 to 85 percent of what they collect in premiums on medical care or improved health. There are many potential pitfalls in his, including decisions as to what expenses are included in the 80 to 85 percent. But if this provision really is enforced, the Affordable Care Act could be an improvement over the existing system.

But the new law couldn’t work without the mandate that every individual be required to buy health insurance. Otherwise the only people in the system would be poor, sick people, and premiums would have to be enormous.

Back in the glory days of Eastman Kodak Co., the Rochester, N.Y., was considered a model for health insurance. Hillary Clinton came to Rochester to call attention to our good system. What made it work was that Eastman Kodak Co. allowed its employees to be insured in a community-wide system. Because Kodak employees were healthy and solvent, that lowered the overall cost of insuring the people of the community. Later, when Kodak fell on hard times, the company withdrew and set up its own health insurance system. And now, with the company in bankruptcy proceedings, many of my friends who’ve retired from Kodak are worried about whether they’ll keep their health insurance. I think it is unrealistic and unfair to saddle private corporations with responsibility for public welfare unrelated to their business. But that’s another story.

Click on Patient Protection and Affordable Care Act wiki for Wikipedia’s excellent explanation of the provisions of this complicated law.

Click on Medical Loss Ratio: Getting Your Money’s Worth on Health Insurance for an explanation of the Affordable Care Act’s provisions requiring 80 to 85 percent of premiums be used for actual medical and health costs.

Click on Supreme Court and Obamacare for an argument as to why the Affordable Care Act is constitutional.

Click on Obamacare Has Already Transformed U.S. Health Care for Business Week’s analysis of the impact of the Affordable Care Act.

Click on What Mitt Romney Would Do In Place of Obamacare for a speculative article analyzing Governor Romney’s campaign statements.

Click on Why I Do Not Like Providing Health Insurance to My Employees for an argument against employer-provided health insurance.

| Word from the Dark S… on Nina Paley’s “This… | |

| jonangel on Can the USA ever end its … | |

| silverapplequeen on Can the USA ever end its … | |

| Anonymous on A Chinese artist’s memoi… | |

| whungerford on How CIA manipulated press cove… | |

| Fred (Au Natural) on Use NATO troops or face humili… | |

| Anonymous on Looking at the sun | |

| Alex Page on Wait, wait, wait! Maybe it… | |

| Bill Harvey on Wait, wait, wait! Maybe it… | |

| Heineman, Robert A on Wait, wait, wait! Maybe it… | |

| lobotero on Wait, wait, wait! Maybe it… | |

| gerrydunphy on Wait, wait, wait! Maybe it… |